From Form to Substance: The Next Chapter of Japan's Governance Reforms

2026年4月20日

Anuja Agarwal, Head of Research for Japan and India of the Asian Corporate Governance Association (ACGA)

Over the past decade, Japan's corporate governance reforms have moved from aspiration to visible market impact. Equity prices, international capital flows, and global rankings now reflect a governance ecosystem that is considerably stronger than in the early days of Abenomics. At the same time, investor expectations have risen in parallel. Directors now face a different question: not "Do we comply?" but "Are we using governance as a strategic lever for long-term value creation?"

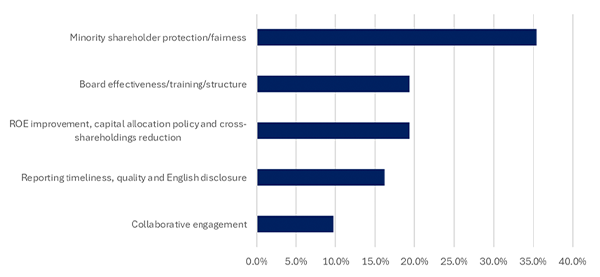

Against this backdrop, the Asian Corporate Governance Association (ACGA) conducted a survey1 of its Japan Working Group (JWG) institutional investor members following its annual Japan delegation in October 2025. The results highlight priorities that are particularly relevant to corporate directors: strengthening minority shareholder protection in takeover and buyout situations and enhancing board effectiveness and leadership. Both issues go to the heart of trust in the board as an effective steward of the company's future.

Figure 1: Results of ACGA JWG investor survey 2025

Source: ACGA Research

Boards to Strengthen Minority Investors' Rights

Current law and regulations2 allow boards to remain neutral in the face of a tender offer bid (ToB). As the recent Toyota Industries case shows, special committees are not under a clear fiduciary duty to recommend for or against an offer, even when the interests of minority shareholders are at stake. In practice, this often leaves minority investors without a clear signal from the board about whether the proposed transaction is in their best interests. In many jurisdictions, boards are expected to provide a reasoned opinion on the fairness and strategic rationale of a bid. For Japanese boards, the practical implication is straightforward: special committees must be equipped and mandated to protect minority shareholders, not merely validate process.

Respondents to our survey emphasized that special committees should comprise members with strong financial literacy and experience in evaluating valuation methodologies, capital structure, and deal terms. This is not only about avoiding legal challenge; it is about demonstrating to all stakeholders that the board takes its stewardship role seriously. In short, minority protection in control transactions3 such as ToBs and conflicted acquisitions is not solely a question for policymakers. Boards can already adopt higher standards by:

- Mandating special committees to issue explicit recommendations on deal terms.

- Ensuring that committee members possess the financial expertise to scrutinize valuations and fairness opinions and not be overly reliant on management-selected advisors.

- Clearly disclose the process for evaluating offers, including any alternative options considered.

These practices would bring Japanese boards closer to global best practice and support the broader aim shared by JACD and ACGA of enhancing investor trust as a foundation for sustainable growth.

Board Effectiveness and Leadership: From Structure to Behavior

The second theme that emerges strongly from our investor survey is the need to deepen board effectiveness and independent oversight. Japan has made impressive progress on structural indicators: more than 90% of Tokyo Stock Exchange (TSE) Prime Market companies now have at least one-third independent directors, and over 85% have established nomination and compensation committees4. Yet structures alone do not guarantee effective oversight or high-quality decision-making.

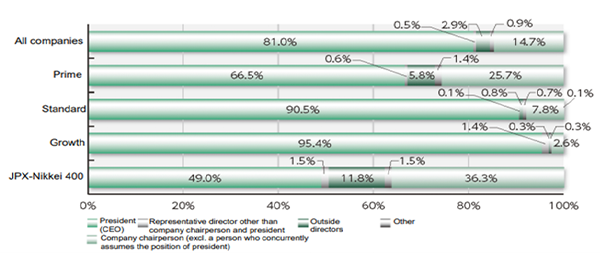

One area of concern is board leadership. According to a TSE white paper published in 20255, only 2.9% of companies currently have an outside director chairing the board. Many boards continue to be led by executive chairs or former CEOs who remain in senior advisory roles, blurring the line between oversight and execution. While such arrangements may feel comfortable within long-standing corporate cultures, investors increasingly view them as obstacles to robust challenge and independent judgment on the board.

Figure 2: Attributes of a Board chair from TSE White paper, 2025

Investors in our survey support a gradual transition toward independent chairs or, at a minimum, the appointment of a strong lead independent director with a clear mandate. This is consistent with JACD's longstanding emphasis on clarifying the oversight role of outside directors and building boards that can both support and challenge management in the interest of sustainable corporate value. An independent chair or lead independent director can:

- Set board agendas that prioritize strategic issues, risk, and capital allocation.

- Ensure that CEO and senior management evaluations are conducted objectively.

- Serve as a focal point for investor engagement, particularly in the absence of a fully independent chair.

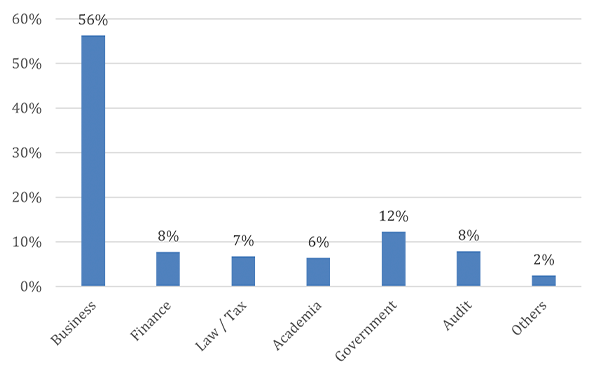

Another pillar of effective boards is human capital development at the director and management levels. Our survey suggests strong investor backing for mandatory and iterative training programmes for directors covering emerging risks, technological change, sustainability issues, and capital market expectations. For Japanese boards, this aligns closely with JACD's educational mission and its commitment to improving the quality of directorship through seminars, publications, and policy work. Well-designed training is not a compliance exercise; it equips directors of diverse backgrounds with tools to navigate increasingly complex strategic issues which may impact company prospects.

Figure 3: Background of Outside Directors for Topix100 companies

Source: UBP Investments Bloomberg Data, December 2025, ACGA Research

Transparency around board performance is another area where Japanese practice lags regional peers. Many companies now conduct board evaluations, yet disclosures often remain high-level, with generic statements that the board is "effective" and limited information on findings or follow-up measures. Investors would like to see more meaningful narrative disclosure: what themes emerged from the evaluation, what specific improvements were identified, and how the board plans to address them over time.

Finally, investor access to independent non-executive directors (INEDs) is viewed as a practical lever to strengthen accountability. Facilitated dialogue with INEDs can give investors insight into how the board thinks about capital allocation, strategy, and succession, beyond what is visible in management presentations. Establishing regular opportunities for such interaction, within appropriate confidentiality boundaries, can reinforce the message that the board welcomes constructive challenges and values the perspectives of long-term shareholders.

Looking Ahead: Directors at the Centre of the Next Phase

Japan's governance reforms have reached a stage where the most important advances will come less from new rules and more from how boards interpret and apply them. The 2023 Action Program for Accelerating Corporate Governance Reform launched by the Financial Services Agency explicitly aims to move from "form to substance," focusing on value creation, capital efficiency, and investor trust. For directors, this is an invitation to go beyond minimum compliance and view governance as an integral part of corporate strategy.

Strengthening minority shareholder protection in control transactions and enhancing board effectiveness and leadership are two areas where boards can have immediate impact. Together, they reflect the ethos shared by JACD and ACGA: governance as an evolving practice that underpins sustainable, long-term growth for companies, markets, and the broader economy.

As Japan works toward revising its Corporate Governance Code and Companies Act this year, the choices made in boardrooms will be as important as those made at the regulatory level. Directors who embrace higher standards of fairness, transparency, and independent oversight will not only help close the gap between regulation and practice but will also position their companies as leaders in the next chapter of Japan's governance story.

NOTE

- https://www.acga-asia.org/advocacy-detail.php?id=529&sk=&sa=

- Japanese law (Companies Act) imposes no fiduciary duty requiring boards to recommend for or against a tender offer (ToB, or takeover bid). TSE's Code of Corporate Conduct (revised July 2025 ) requires special committees (independent outsiders/experts) to opine on whether MBOs/ToBs undermine minority interests, with boards disclosing this fully and explaining decisions. METI's Fair M&A Guidelines and Takeover Guidelines urge boards to form clear opinions (support/oppose/neutral) with rationale, prioritizing corporate value and minority protection, but neutrality remains permissible

- Control transactions involve a party seeking majority ownership or influence, often triggering "entire fairness" review under heightened scrutiny for fairness in price and process. Examples include TOBs, where an acquirer publicly bids for shares to gain control (e.g., bypassing management for a hostile takeover), and conflicted acquisitions like management buyouts (MBOs), controlling shareholder freeze-outs of minorities, or related-party mergers

- https://www.fsa.go.jp/en/refer/councils/follow-up/material/20230419-03.pdf

- https://www.jpx.co.jp/english/equities/listing/cg/tvdivq0000008jb0-att/vk0khi0000002vfp.pdf

Anuja Agarwal Anuja is Head of Research for Japan and India of the Asian Corporate Governance Association (ACGA). She has 20+ years of experience in financial markets and is passionate about integrating ESG strategies with fundamental views and has experience in PRI Disclosures, Stewardship and Proxy voting. She has been on the Board of Zubin Foundation, mentor for 100 women for Finance (100WF) and a Board advisor for a reusable cutlery company Recube.hk. She is a ESG CFA certificate holder and a Talent4Impact Fellow. She is a fitness freak and has completed Greenpower (50k), Moon trekker (42k), UNICEF (20k) races. Her work on financial literacy for kids has been featured on Forbes, SCMP, Radio HK.

これまでの記事[ OPINION ]

- ガバナンス改革、アジアを見渡せ

- 社外取締役受難の時代到来か

- ハーバードから見た日本のCG

- 未上場企業におけるコーポレートガバナンスの提言

- M&A 20年間の変化と原動力

- From Form to Substance: The Next Chapter of Japan's Governance Reforms

- 略語「超」解説:RIM(残余利益モデル)

- 広がる 「親子上場」を 解消する動き

- 社外取締役の機能不全を回避するための施策

- 女性活躍推進ワーキンググループ活動報告

- 多様性がもたらす企業価値向上

- 取締役会5原則とCGガイダンス

- 略語「超」解説:DCF法(ディスカウント・ キャッシュフロー法)

- 経済界の平和への貢献とESGP

- 第三者委員会の有用性と限界を考える

- 消費減税に逃げ込む政治の危うさ

- 独立社外役員から成る調査委員会の妥当性

- AI時代の企業価値向上に向けて~トランスコスモスの挑戦

- ICGN 30th Anniversary Conference Asia: An exciting time for Corporate Governance in Japan

- 略語「超」解説:DDM (配当割引モデル)

- 親会社の社外取締役の役割と責任

- Corporate Governance Needs to Start with "Why"

- 日本の株式市場の変革をもたらす「三点セット」

- 吹き荒れるトランプ旋風

- コーポレートガバナンス改革の「実践」に向けて

- トランプ2.0、日本への余波

- 略語「超」解説:WACC(加重平均資本コスト)

- 社外取締役はガバナンス粉飾に加担するな

- 労働市場改革が宙に浮く懸念

- 人的資本経営におけるジョブ型雇用

- 味の素グループ 企業価値向上の処方箋

- 略語「超」解説:ROIC(投下資本利益率)

- 不祥事企業の社外取締役

- 株式市場で広がる「同意なき買収」

- 何が日本的経営を腐食させたか

- トップマネジメントとして備えたい「伝える力」

- 株主・投資者の目線を踏まえた経営の実現に向けて

- Purposeを起点とした価値創造とコーポレートガバナンス

- 略語「超」解説:PBR(株価純資産倍率)

- 社外取締役の説明責任

- 政策保有株の売却が加速

- 人的資本経営ブームの本当の捉え方

- 地政学リスクの時代の企業価値向上

- ACGA's market rankings for corporate governance

- 人材育成を経営戦略に生かせ

- コーポレートガバナンスの真意の共有

- 不祥事対応のリスクマネジメント~第三者委員会・調査委員会とガバナンス

- 社外取締役のトレーニングと買収行動指針

- 資産運用立国

- 指名委員会こそ、健全なガバナンス構築の根幹

- 政府が女性役員の登用で数値目標

- 人的資本経営における「安心」と確定拠出年金(DC)

- コーポレートガバナンス改革の実質化に向けて

- 事業を通じて世の中の課題解決に貢献する

- 我が国のベンチャー・エコシステムの高度化に向けた提言

- 企業価値向上とESG投資

- 不毛な「守り」と「攻め」のガバナンス議論

- サステナビリティ経営に資するコーポレートガバナンス

- グローバル投資家の視点から見た日本のコーポレートガバナンス改革

- 気候変動への取組みは待ったなし~世界の最新動向

- 「金融と 財政の悪循環」を断ち切れ

- ガバナンス議論の神髄をなすアカウンタビリティー

- CGSガイドラインの改訂で議論された方向性について

- コーポレートガバナンスとパッシブ運用

- コロナ特例 「ゼロゼロ融資」が終了

- 義務教育DXとガバナンス

- ガバナンス議論の原点を振り返る

- コーポレートガバナンス改革の点検と非財務情報開示の充実について

- 日本も財政検証機関の設立を

- 企業理念(hhc理念)とコーポレートガバナンス

- モニタリング・モデルを採用する会社における監査委員会等の監査について

- 事業法人は公益法人と協働を

- コロナ禍があぶり出した課題

- 東京証券取引所の 市場再編

- リナ・カーンの戦い

- 今後のコーポレートガバナンス改革の取組みについて

- 持続性が問われる「資本主義」

- コーポレートガバナンスを担保するのは経営者の高い志と倫理観

- 日本の製造業の展望と課題

- 危機管理としての 財政健全化

- 新市場区分と改訂コーポレートガバナンス・コードの下での企業価値向上

- コーポレートガバナンスを考えることは、経営の基本

- デジタル化と規制改革

- 社外取締役の 獲得競争が激化

- なぜ「コーポレートガバナンス」なのか

- 新型コロナウイルスと 日本における 株主アクティビズム

- 新政権の突破力が問われる労働規制改革

- 企業不祥事と 「タコツボ」

- いま求められるコーポレートガバナンスの深化

- 日立の取締役会改革

- 行政のデジタル化を規制改革の起爆剤に

- 「良き資本主義」を実現する ボトムライン革命

- 両利き経営を実現する コーポレート・ トランスフォーメーション

- 証券取引等監視委員会の活動方針

- コーポレートガバナンスの深化と市場の評価

- 次期会社法改正に向けての課題

- コーポレートガバナンス改革の今後の動向

- 新型肺炎が突きつける日本型システムの脆弱性

- 変容する米企業の株主第一主義

- 老後2000万円問題の本質

- 外為法改正の外資規制企業統治改革に逆行も

- Do the right thing ~形式と実質~

- 緊張感に包まれた歴史的な株主総会